This is paragraph text. Click it or hit the Manage Text button to change the font, color, size, format, and more. To set up site-wide paragraph and title styles, go to Site Theme.

February 2026 Newsletter

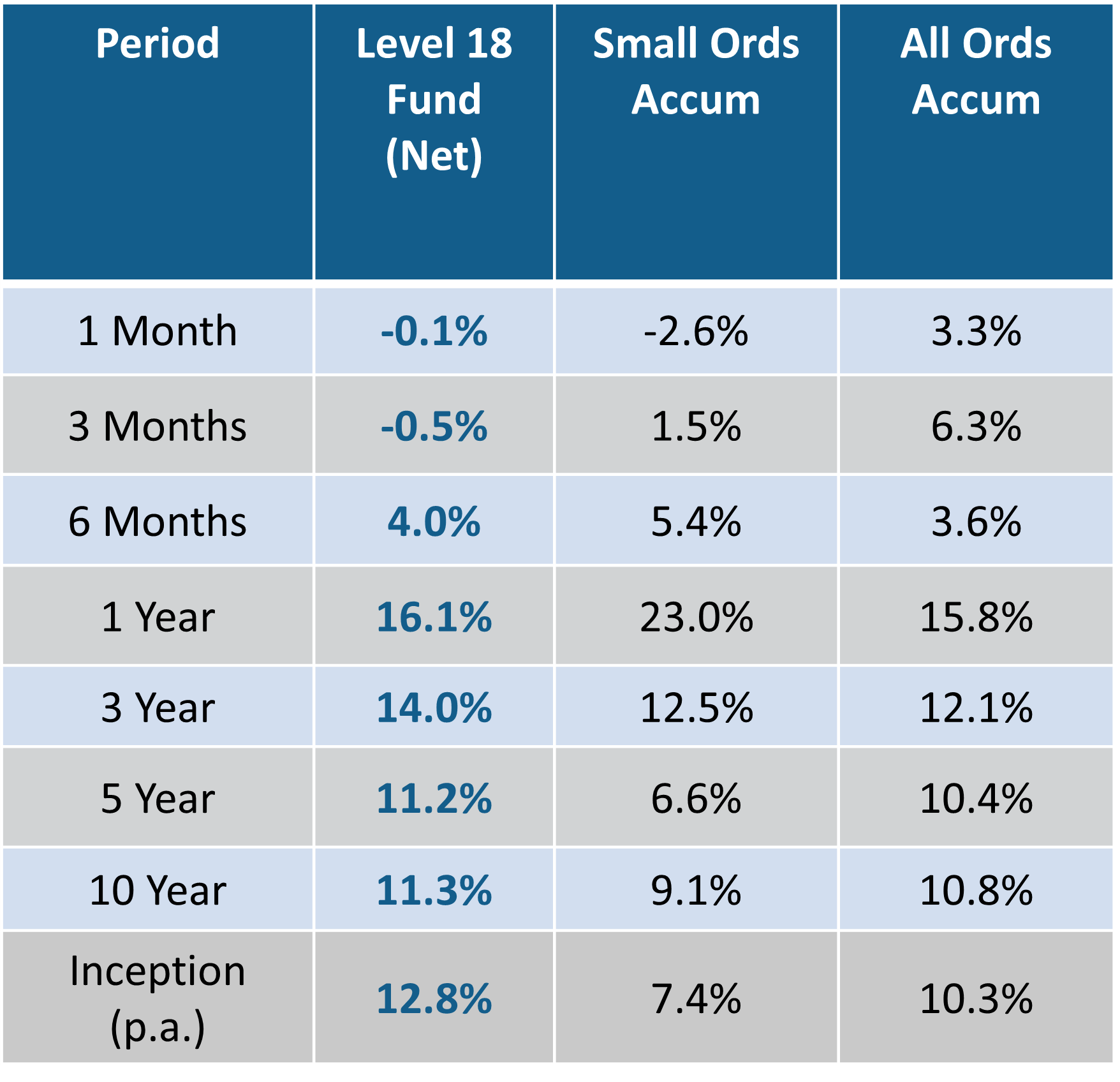

The Level 18 Fund decreased by -0.1 per cent net of fees for the month.

Commentary

The Level 18 Fund decreased by -0.1 per cent net of fees for the month. For the 12 months to February 28, 2026, the Fund increased by +16.1 per cent.

February was a mixed month across global equities as investors balanced the risks associated with inflation, corporate earnings and shifting central bank policy. The potential for further geopolitical instability in the Middle East also weighed on investor sentiment. Post the month end, the US and Israel launched strikes on Iran following the breakdown of nuclear negotiations.

February was a positive month for large cap equities in Australia where the All-Ordinaries Accumulation Index increased by +3.3 per cent. In contrast, the S&P/ASX Small Ordinaries Accumulation Index declined by -2.6 per cent. Small cap resources again outperformed in February with the sector up +0.8 per cent for the month. Small cap industrials were down -4.8 per cent.

In Australia, the Banking sector made the largest contribution to the market’s positive performance. Mining was the next largest contributor. Health was the worst sector due to disappointing results and moderating growth. Specifically, Banks and Mining were up +13.5 per cent and +9.4 per cent respectively. Healthcare was down -13 per cent in the month. Large Caps dominated the month with Commonwealth Bank (CBA) up +18 per cent and BHP Group (BHP) up +17 per cent respectively.

The US market was slightly negative in February. Investors rotated capital away from AI-related and growth exposed sectors and into Industrials, Financials, Energy and Consumer Staples.

The S&P 500 and the Nasdaq Composite Index finished the month down -0.9 per cent and -3.4 per cent respectively. The Russell 2000 (US small caps) continued to outperform in the month, up +0.7 per cent.

Portfolio holding Clearview Wealth (CVW) performed well in February. The company entered into a scheme implementation deed with Zurich Financial to acquire 100% of CVW. Under the scheme, CVW shareholders will receive $0.65 per share. The company Directors have recommended the transaction in the absence of a superior offer. The consideration represents a 21.5 per cent premium to the CVW closing price on Feb 23, 2026.

The Australian 1H FY26 reporting season delivered significant share price volatility. Company earnings and outlook statements that missed expectations were sold aggressively. However, across the market company results were genuinally solid. According to Macquarie research, 32 per cent of company’s ‘beat’ consensus expectations and 20 per cent ‘missed’.

History has taught us that the share price increases associated with strong results tend to continue over several months post the initial outperformance. As a result, we have taken the opportunity to selectively add to portfolio positions where results were better-than-expected. For example, Superloop (SLC) has recently been added to the portfolio following a good result.

The company delivered strong subscriber growth that drove revenues up +23 per cent and underlying EBITDA up +46 per cent. The company delivered operating margin expansion and scale benefits during the period. Importantly, cash conversion was also strong.

Post the result, underlying EBITDA guidance for FY26 was increased and we see the FY26 earnings target as being conservative.

SLC’s announced acquisition of Lightning Broadband is expected to strengthen the company’s market position in the “Fibre-To-The-Premises” market and accelerates its growth within the company’s “Smart Communities” division.

Positive contributors to the Fund’s performance in February include civil, resource and infrastructure services group NRW Holdings (NWH), construction materials and building product producer Wagners Holding (WGN), power distribution and industrial communications group IPD Group (IPG) and life insurance product provider Clearview Wealth (CVW).

Household furniture retailing group Nick Scali (NCK), equipment financing and broking business COG Financial Services (COG) and Integrated retirement village service provider Summerset Group (SUM) made negative contributions to performance in the month.

The Level 18 Fund Information Memorandum (IM) and application form are available on the Centennial Asset Management website. Please note existing unit holders are only required to compete a one-page additional application form. The following link (https://www.centennialfunds.com.au/) provides access to the IM and application documents.

Thank you as always for your continued support and please contact Michael Carmody (mcarmody@centennialfunds.com.au or +61 2 8071-9215) if you would like any further details.

The Centennial Team

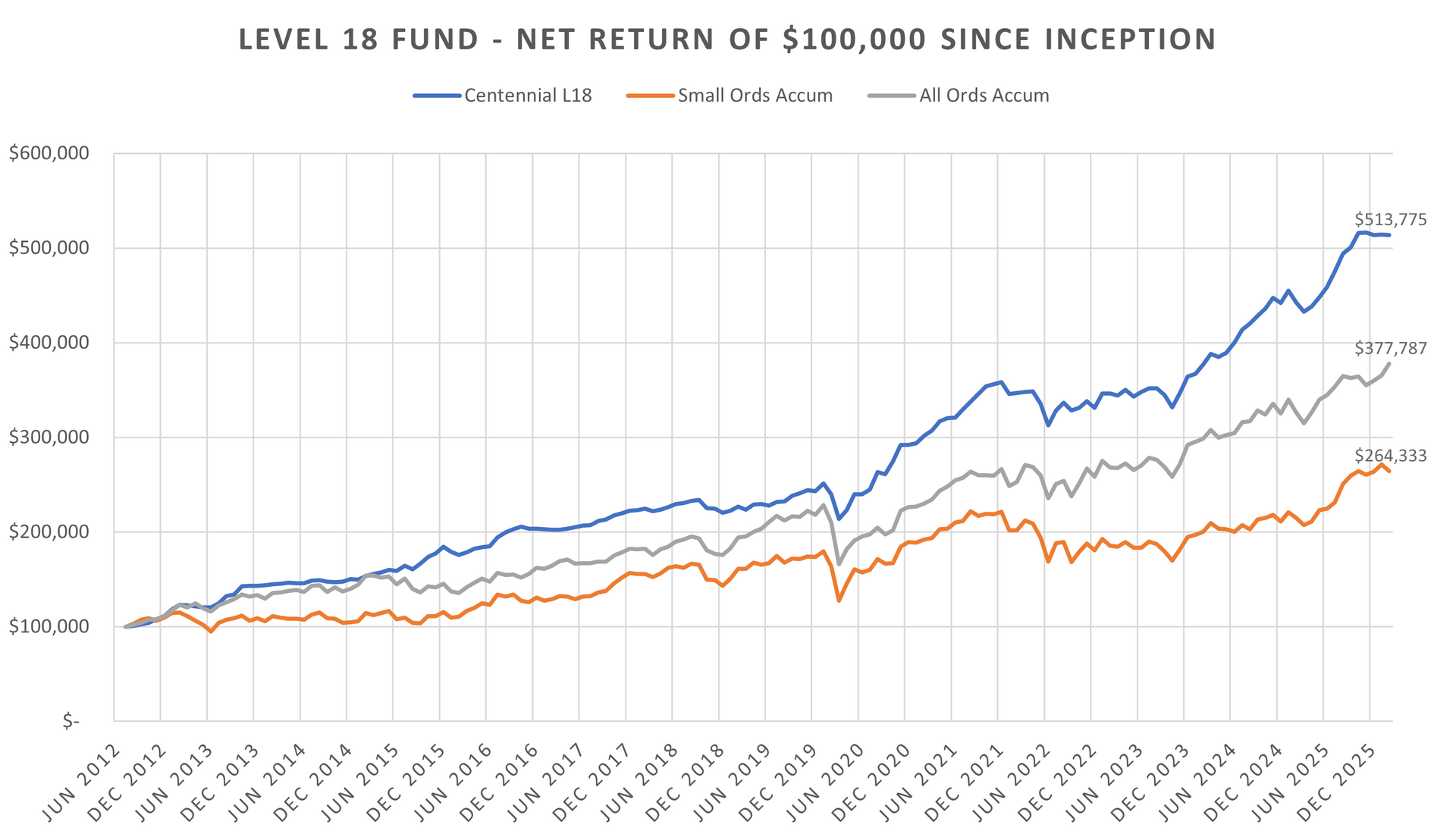

Monthly Net Returns Since Inception

About Centennial Asset Management

Centennial Asset Management is an independent Australian asset management business, and the manager of the Level 18 Fund, an index unaware fund, with asset allocation flexibility and a concentration of small capitalised companies. Further information on Centennial is available on our website - www.centennialfunds.com.au

Disclaimer

Strictly confidential: This report has been prepared by Centennial Asset Management ACN 605 827 745 & AFSL No. 515887 for Wholesale Clients only as an indicative record of the performance of an investment in the Level 18 Fund. No recommendation is made or advice given in respect of any entity in which the Level 18 Fund has, is or may in the future be, invested. The contents of this report are confidential, and the client may only disclose such contents to its officers, employees or advisers on a need to know basis, or with the prior written consent of Centennial Asset Management. Centennial Asset Management does not guarantee the performance of the Level 18 Fund or the return of any investor's capital in the Level 18 Fund. This investment report contains historical information, and does not imply any indication of future performance, recommendation or advice. Past performance is not a reliable indicator of future performance. Any investment needs to be made in accordance with and after reading any relevant offer document. This material has been prepared based on information believed to be accurate at the time of publication. Assumptions and estimates may have been made which may prove not to be accurate. Centennial Asset Management accepts no responsibility to correct any such inaccuracy. Subsequent changes in circumstances may occur at any time and may impact the accuracy of the information. To the full extent permitted by law, none of Centennial Asset Management, or any related body corporate or any officer or employee of any of them makes any warranty as to the accuracy or completeness of the information in this report and disclaims all liability that may arise due to any information contained in this newsletter being inaccurate, unreliable or incomplete. *Prior to launch of the Level 18 Fund on 1 September 2014, Centennial Asset Management had established a separately managed account (“SMA”) and performance prior to 1 September 2014 is illustrated on a gross pro-forma basis, that invests with the same mandate as the Level 18 Fund and is included in the tables above, for comparative purposes only. The returns assume reinvestment of distributions.