This is paragraph text. Click it or hit the Manage Text button to change the font, color, size, format, and more. To set up site-wide paragraph and title styles, go to Site Theme.

March 2026 Newsletter

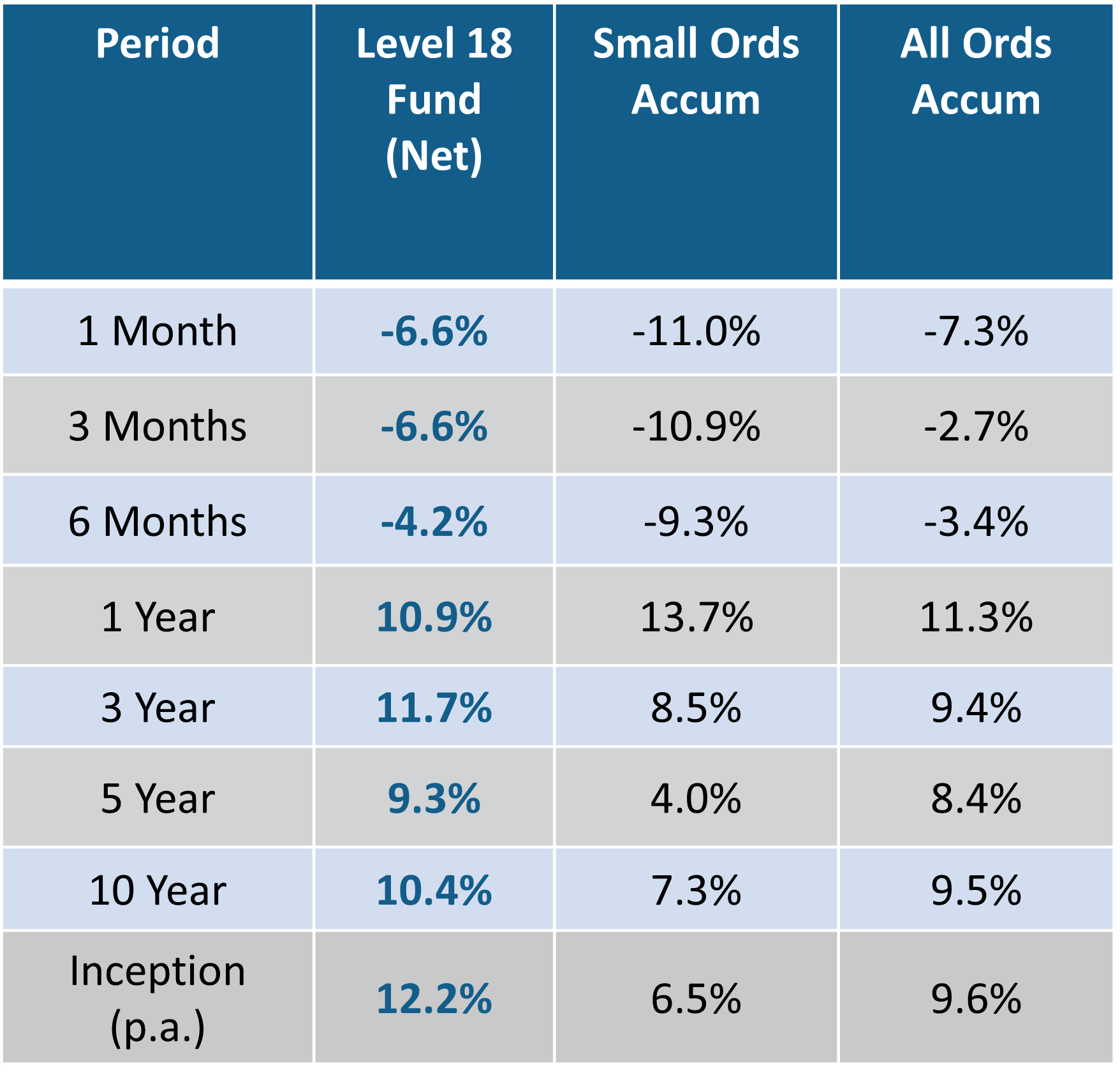

The Level 18 Fund decreased by -6.6 per cent net of fees for the month.

Commentary

The Level 18 Fund decreased by -6.6 per cent net of fees for the month. For the 12 months to March 31, 2026, the Fund increased by +10.9 per cent.

In the US, the S&P 500 and the Nasdaq Composite Index finished the month down -5.1 per cent and -4.8 per cent respectively. The Russell 2000 (US small caps) was down -5.2 per cent.

During March, headlines associated with the latest conflict in the Middle East dominated global equity markets. The biggest impact was the rapid rise in oil prices which increased by approximately 50 per cent since the conflict began. In addition, US 10-year bond yields rose sharply during the month and finished at 4.32 per cent compared to 3.96 per cent at the end of February.

March was a negative month for global equities as investors lowered risk and allocated capital to defensive exposures. US and European equity markets were relatively resilient during the month in contrast to Asian markets where energy import dependence is significantly higher. Global defence, aerospace, energy and commodity sectors outperformed while airline, travel, and consumer discretionary sectors underperformed. Towards the end of the month as headlines emerged regarding a potential ceasefire, oil prices declined and global markets delivered a modest relief rally.

The war in Iran is set to deliver elevated energy costs, inflation risks and constraints on global economic growth for a period. The ultimate impact is dependant on the length of the conflict and how long shipping traffic in the Strait of Hormuz is restricted. As a result, stock positioning within the Centennial Level 18 portfolio has changed to protect capital and optimise performance.

The fund carried structurally higher levels of cash during the month. Exposure to interest rate sensitive (property trusts, debt providers & banks) and consumer discretionary (retail) sectors were lowered and companies with lower-risk capex exposed earnings growth (mining services, engineering contractors and data centres) were prioritised.

In Australia, March was a negative month for both large and small caps. The large cap market delivered its largest drawdown since June 2022. The All-Ordinaries Accumulation Index and the S&P/ASX Small Ordinaries Accumulation Index declined by -7.3 per cent and -11.0 per cent respectively. In contrast to the previous month, Small cap resources underperformed in March with the sector down -15.4 per cent for the month. Small cap industrials were down -9.3 per cent.

The March sell-off was dominated by growth stocks (Wisetech Global & Goodman Group) as inflation risks delivered higher bond yields (10-year peaking at +5.0 per cent) and investors de-risked equity exposures.

Consumer discretionary, Information technology and Materials made the largest negative contributions to the small cap sector. While Energy, Communication services and Consumer Staples made positive contributions.

During the month the RBA elected to increase interest rates by 25 bps to 4.10 per cent. The move higher for the second straight meeting in response rising inflation which risks being exacerbated by the increased energy costs associated with the conflict in the Middle East. Inflation currently sits at 3.8 per cent, above the target range of 2 to 3 per cent. The RBA noted that, “higher prices and prolonged uncertainty may cause growth to be lower in Australia’s major trading partners and also in Australia.”

As widely expected, the US Fed kept rates on hold primarily because policymakers are facing conflicting economic signals and high levels of uncertainty regarding the outlook for the US economy.

Positive contributors to the Fund’s performance in March include telecommunication and internet service provider Superloop (SLC), supermarket retail store group Woolworths (WOW), wireless technology & communication group Etherstack (ESK) and petroleum product and retail convenience company Ampol (ALD).

Power distribution and industrial communications group IPD Group (IPG), civil, resource and infrastructure services group NRW Holdings (NWH) and maintenance & construction group Monadelphous (MND) made negative contributions to performance in the month.

The Level 18 Fund Information Memorandum (IM) and application form are available on the Centennial Asset Management website. Please note existing unit holders are only required to compete a one-page additional application form. The following link (https://www.centennialfunds.com.au/) provides access to the IM and application documents.

Thank you as always for your continued support and please contact Michael Carmody (mcarmody@centennialfunds.com.au or +61 2 8071-9215) if you would like any further details.

The Centennial Team

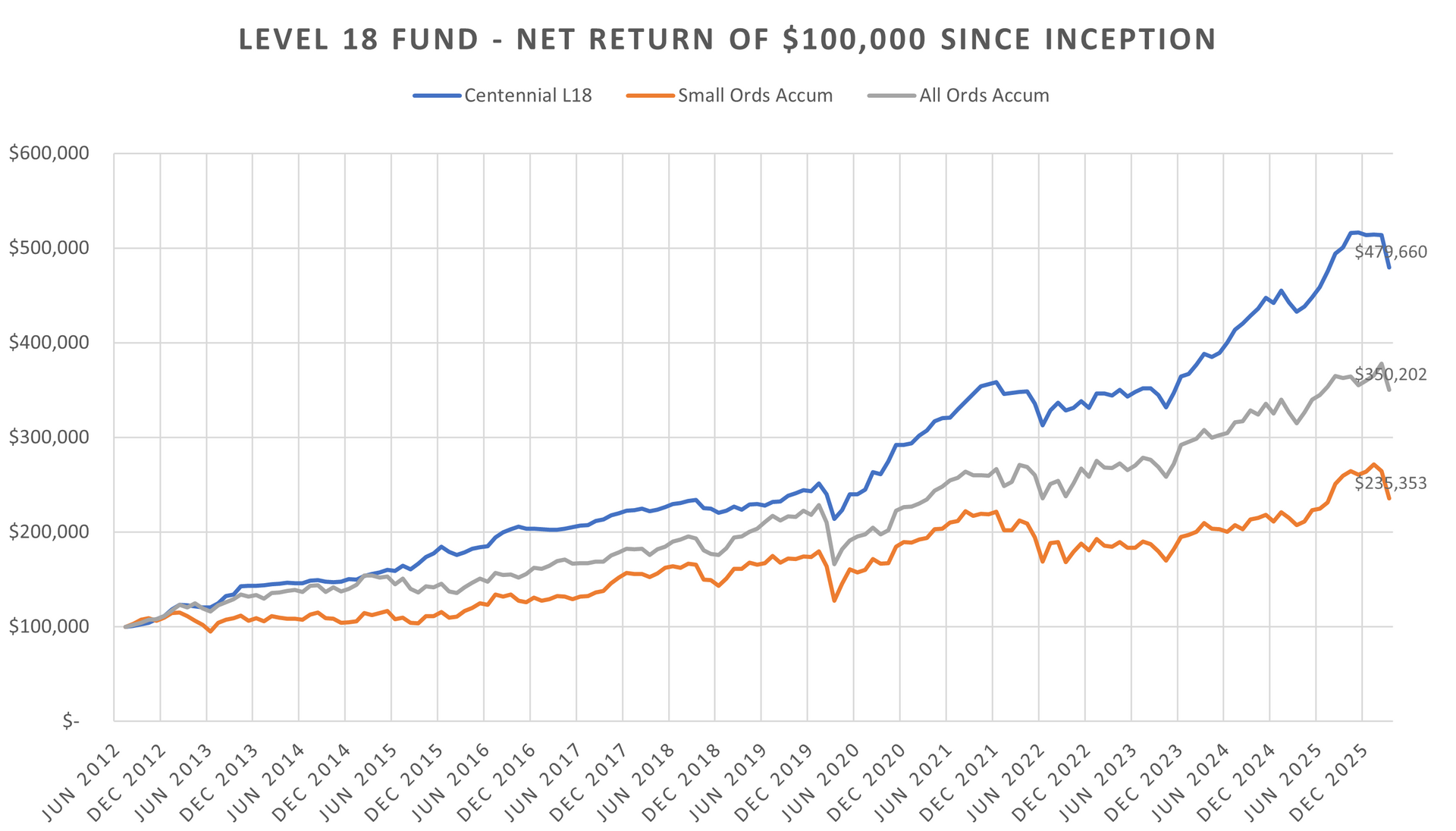

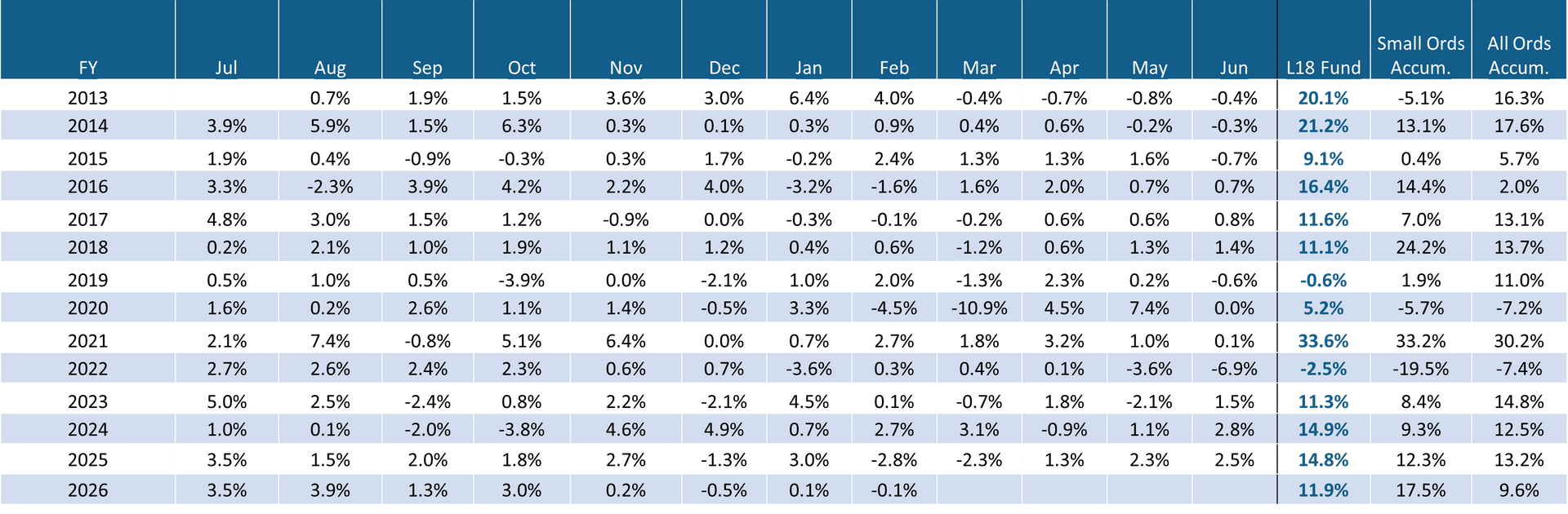

Monthly Net Returns Since Inception

About Centennial Asset Management

Centennial Asset Management is an independent Australian asset management business, and the manager of the Level 18 Fund, an index unaware fund, with asset allocation flexibility and a concentration of small capitalised companies. Further information on Centennial is available on our website - www.centennialfunds.com.au

Disclaimer

Strictly confidential: This report has been prepared by Centennial Asset Management ACN 605 827 745 & AFSL No. 515887 for Wholesale Clients only as an indicative record of the performance of an investment in the Level 18 Fund. No recommendation is made or advice given in respect of any entity in which the Level 18 Fund has, is or may in the future be, invested. The contents of this report are confidential, and the client may only disclose such contents to its officers, employees or advisers on a need to know basis, or with the prior written consent of Centennial Asset Management. Centennial Asset Management does not guarantee the performance of the Level 18 Fund or the return of any investor's capital in the Level 18 Fund. This investment report contains historical information, and does not imply any indication of future performance, recommendation or advice. Past performance is not a reliable indicator of future performance. Any investment needs to be made in accordance with and after reading any relevant offer document. This material has been prepared based on information believed to be accurate at the time of publication. Assumptions and estimates may have been made which may prove not to be accurate. Centennial Asset Management accepts no responsibility to correct any such inaccuracy. Subsequent changes in circumstances may occur at any time and may impact the accuracy of the information. To the full extent permitted by law, none of Centennial Asset Management, or any related body corporate or any officer or employee of any of them makes any warranty as to the accuracy or completeness of the information in this report and disclaims all liability that may arise due to any information contained in this newsletter being inaccurate, unreliable or incomplete. *Prior to launch of the Level 18 Fund on 1 September 2014, Centennial Asset Management had established a separately managed account (“SMA”) and performance prior to 1 September 2014 is illustrated on a gross pro-forma basis, that invests with the same mandate as the Level 18 Fund and is included in the tables above, for comparative purposes only. The returns assume reinvestment of distributions.