This is paragraph text. Click it or hit the Manage Text button to change the font, color, size, format, and more. To set up site-wide paragraph and title styles, go to Site Theme.

September 2025 Newsletter

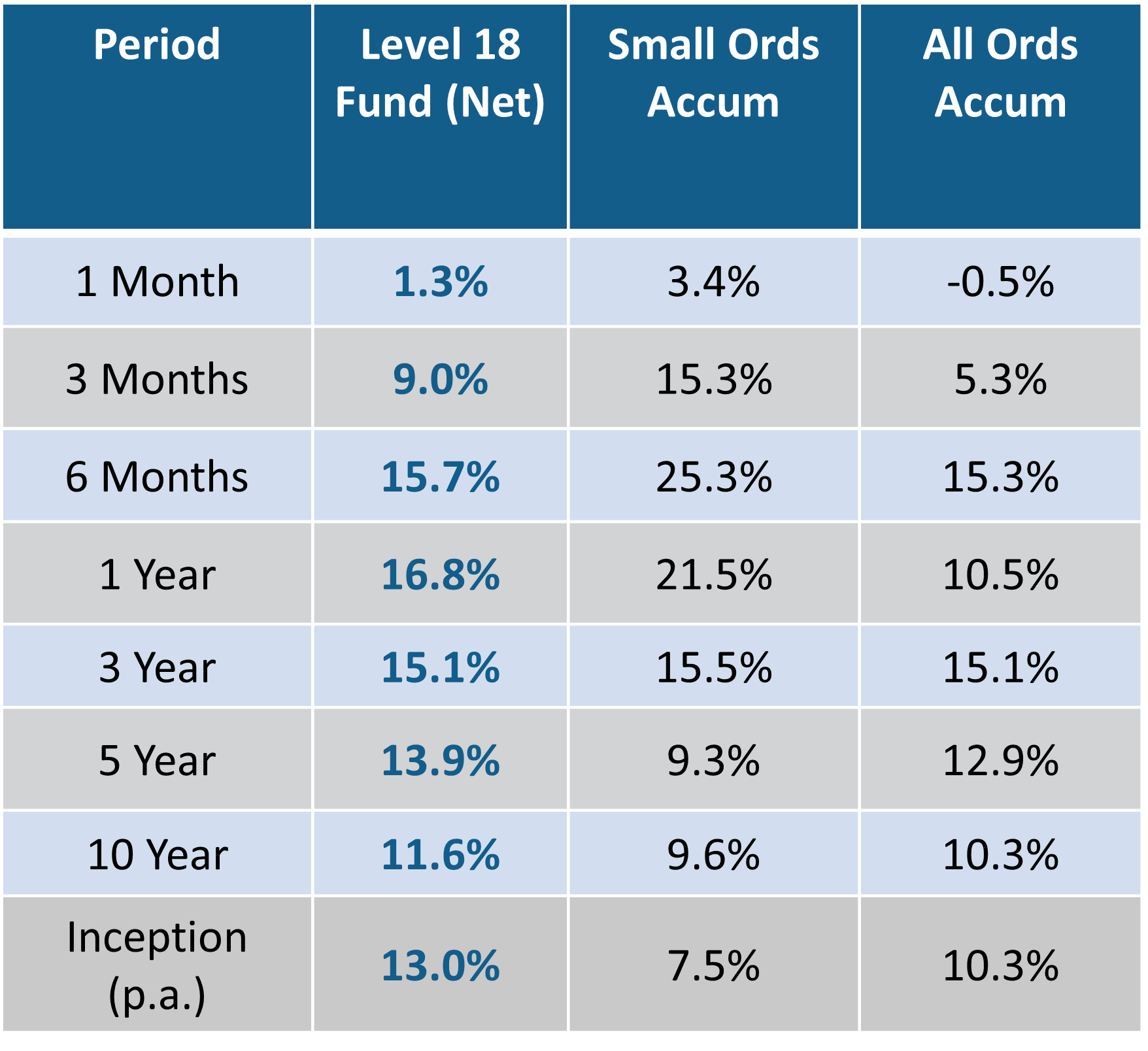

The Level 18 Fund increased by +1.3 per cent net of fees for the month.

Commentary

The Level 18 Fund increased by +1.3 per cent net of fees for the month.

September is traditionally a poor month for global equities. That proved to be the case for the Australian large cap sector. The All Ordinaries Accumulation Index was down -0.5 per cent in the month. In contrast, the US market delivered its best September in 27 years on the back of ongoing investor enthusiasm for AI/semiconductor exposed stocks. The S&P 500 and the Nasdaq Composite Index finished the month up +3.5 per cent and +5.7 per cent respectively.

Like the previous month, the small cap sector outperformed large caps. Specifically, the S&P/ASX Small Ordinaries Accumulation Index increased by +3.4 per cent compared to the All Ordinaries Accumulation Index which was down -0.5 per cent.

The small cap outperformance was driven by a number of Macro and stock-specific issues.

On the Macro front, the three RBA (Reserve Bank of Australia) interest rate cuts are starting to deliver benefits for the economy. Lower rates, moderating inflation and a proportionally higher exposure to domestic demand tend to benefit small caps versus large caps.

On the stock specific front, disappointing FY25 earnings and guidance from a number of companies including CSL, Reece, James Hardie, Dominos, Woolworths and Sonic Healthcare dragged on the large cap sector.

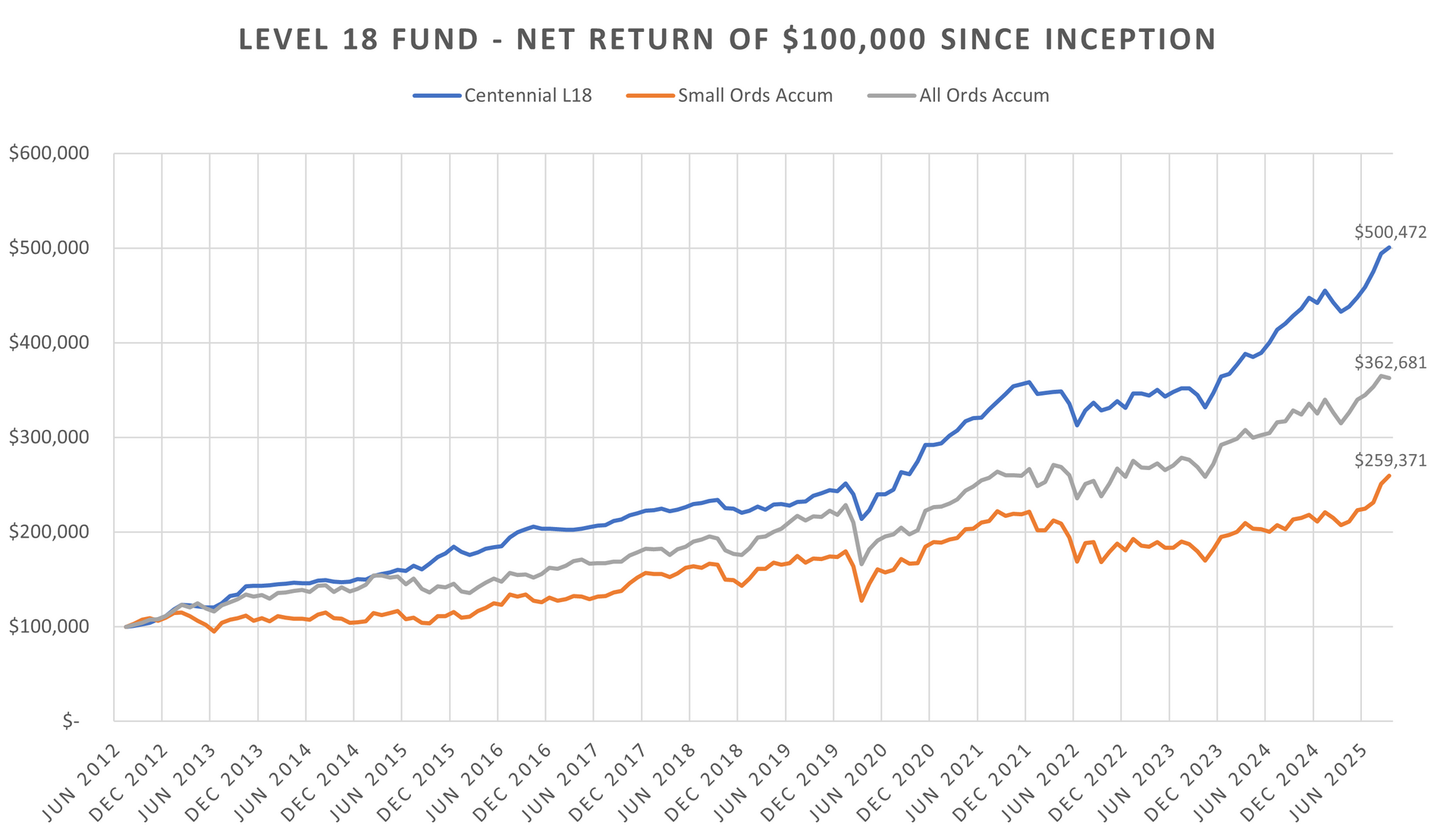

The Centennial Level 18 Fund recently reached its 13th year milestone. The Fund’s flexible mandate protects capital in bad markets and delivers performance in rising markets. Since inception (2012), the Fund has delivered a +13 per cent net return per annum versus the All-Ordinaries Accumulation Index at +10.3 per cent and the S&P/ASX Small Ordinaries Accumulation Index at +7.5 per cent.

We expect small cap outperformance to continue over the next 12-24 months for several reasons.

1. Valuations - Small cap valuations remain attractive. Small caps continue to trade at a discount to large caps. The 12 month forward small cap PER multiple is currently 15.4x versus large caps at 19.8x.

2. Earnings growth - The earning growth outlook for small caps is superior to large caps. Consensus one year forward forecasts expect earnings growth of +13.2 per cent for small caps vs large caps at +2.8 per cent.

3. Exposure to structural growth thematics - We continue to expect small caps to benefit from an expose to several structurally growing sectoral thematics such as data centre expansion, housing price & construction growth and increased defence spending.

In September, following a 25bp cut in August, the RBA elected to leave rates unchanged. It is important to note the Governor’s commentary post the meeting regarding the economic outlook. She specifically observed that GDP has been stronger-than-expected, the labour market resilient and the rising risk of service price inflation. Our base case expectations are unchanged. We expect two further 25bp rate cuts during the next year.

During the month, Level 18 Fund holding, Service Stream (SSM) secured a significant Base Service Contract with the Department of Defence during the month. The company has been appointed to provide Property and Asset Services for 113 Defence sites in SA and the NT. Commencing on the 1 Feb 2026, the Contract will operate for an initial 6-year term, with the option to a maximum term of 10-years. The combined value of the work is approximately $1.6 billion over the initial term. The stock was up +11 per cent in the month.

Post the reporting season, we have added several new exposures that look well positioned to deliver a recovery in earning growth over the next 12-24 months. We continue to identify a number of investment opportunities at attractive valuations. The Fund’s fundamental stock selection and risk management parameters are unchanged.

Positive contributors to the Fund in September include Audio-visual & electrical contractor SKS Technologies (SKS), equipment financing and broking business COG Financial Services (COG), mining software solutions group RPM Global (RUL), specialist alternative investment manager Regal Partners (RPL) and construction and maintenance group GenusPlus (GNP).

Residential aged care home provider Regis Healthcare (REG), Construction contracting, equipment hire and civil remediation services provider Symal (SYL) and online automotive, motorcycle and marine classified business CAR Group (CAR) made negative contributions to the performance in the month.

The Level 18 Fund Information Memorandum (IM) and application form are available on the Centennial Asset Management website. Please note existing unit holders are only required to compete a one-page additional application form. The following link (https://www.centennialfunds.com.au/) provides access to the IM and application documents.

Thank you as always for your continued support and please contact Michael Carmody (mcarmody@centennialfunds.com.au or +61 2 8071-9215) if you would like any further details.

The Centennial Team

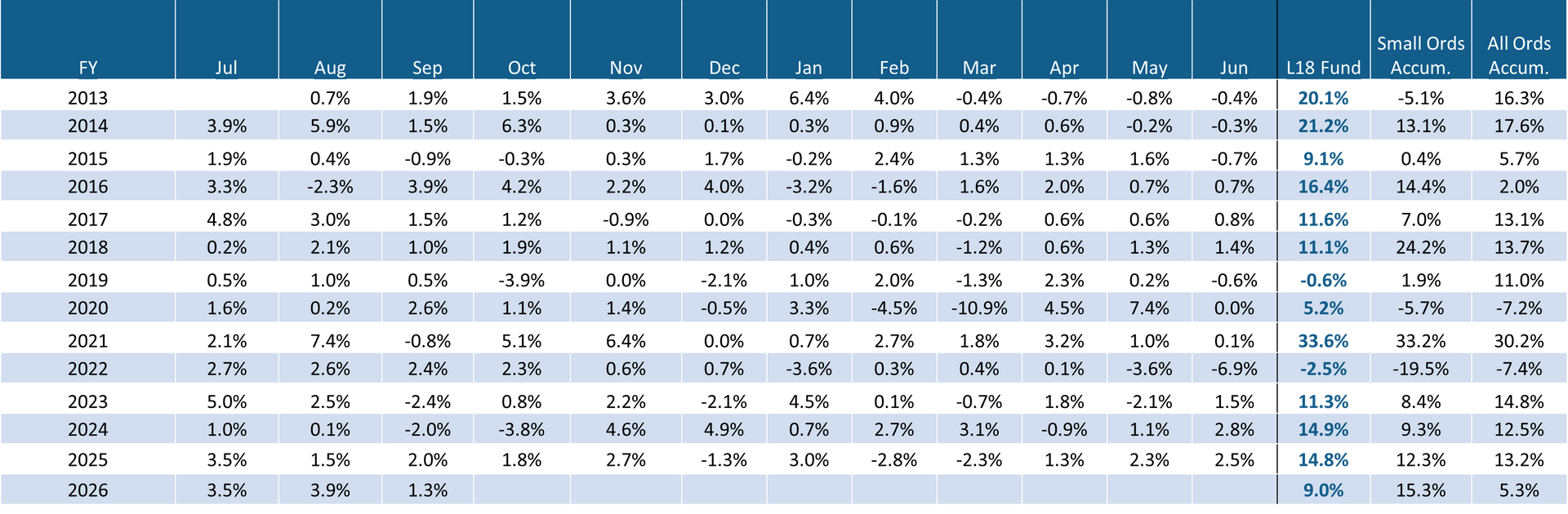

Monthly Net Returns Since Inception

About Centennial Asset Management

Centennial Asset Management is an independent Australian asset management business, and the manager of the Level 18 Fund, an index unaware fund, with asset allocation flexibility and a concentration of small capitalised companies. Further information on Centennial is available on our website - www.centennialfunds.com.au

Disclaimer

Strictly confidential: This report has been prepared by Centennial Asset Management ACN 605 827 745 & AFSL No. 515887 for Wholesale Clients only as an indicative record of the performance of an investment in the Level 18 Fund. No recommendation is made or advice given in respect of any entity in which the Level 18 Fund has, is or may in the future be, invested. The contents of this report are confidential, and the client may only disclose such contents to its officers, employees or advisers on a need to know basis, or with the prior written consent of Centennial Asset Management. Centennial Asset Management does not guarantee the performance of the Level 18 Fund or the return of any investor's capital in the Level 18 Fund. This investment report contains historical information, and does not imply any indication of future performance, recommendation or advice. Past performance is not a reliable indicator of future performance. Any investment needs to be made in accordance with and after reading any relevant offer document. This material has been prepared based on information believed to be accurate at the time of publication. Assumptions and estimates may have been made which may prove not to be accurate. Centennial Asset Management accepts no responsibility to correct any such inaccuracy. Subsequent changes in circumstances may occur at any time and may impact the accuracy of the information. To the full extent permitted by law, none of Centennial Asset Management, or any related body corporate or any officer or employee of any of them makes any warranty as to the accuracy or completeness of the information in this report and disclaims all liability that may arise due to any information contained in this newsletter being inaccurate, unreliable or incomplete. *Prior to launch of the Level 18 Fund on 1 September 2014, Centennial Asset Management had established a separately managed account (“SMA”) and performance prior to 1 September 2014 is illustrated on a gross pro-forma basis, that invests with the same mandate as the Level 18 Fund and is included in the tables above, for comparative purposes only. The returns assume reinvestment of distributions.